The 2018 FIFA World Cup in Russia kicked-off only a few days ago, but the bidding process for sponsor and broadcasting rights was launched long before the start of the biggest global football event.

The previous World Cup, held in Brazil in 2014, generated $4.8 billion in revenues for FIFA, half of which originated from the sale of broadcasting rights, while sponsorship fees accounted for $1.6 billion.

FIFA has already announced it is going to improve on these figures and make an estimated total of $6.1 billion in 2018, 10% more than envisaged.

Revenues from broadcasting rights are expected to exceed the $3 billion target by 2% and sponsorship deals have generated $200 million more than the projected $1.45 billion. Considering the importance of those two revenue streams for the football governing body, in this article KPMG Football Benchmark reviews the most prominent sponsorship and broadcasting agreements made for this year’s World Cup.

Sponsorship

FIFA divides sponsors or so-called partners into three different categories: FIFA Partners; FIFA World Cup Sponsors; and Regional Supporters.

Partners have the highest level of association with FIFA and all of its events and are classified as long-term, strategic agreements that extend beyond the actual tournaments. The World Cup Sponsors have rights to both the Confederations Cup and the World Cup on a global basis. Sponsors at this level benefit from a strong brand association with these two global tournaments, the use of selected marketing assets and media exposure, as well as ticketing and hospitality offers for the events.

The Regional Supporter level was introduced after the Brazil World Cup in 2014 (previously called National Supporters) and is the third level of FIFA’s sponsorship structure, allowing companies within the pre-defined global regions to promote an organization through the World Cup in their domestic markets.

For all of these partnership categories, FIFA has a limit to the number of slots it can allocate. Whereas the Partners and World Cup Sponsors group offers rights to a maximum of eight companies, the Regional Supporters tier is open to 20 partners, with a maximum of four brands per region (Europe, North/Central America, South America, Africa/Middle East, Asia).

After established brands such as Sony, Emirates, Castrol, Continental and Johnson & Johnson failed to renew deals expiring after 2014, Chinese companies stepped-in. In this year’s World Cup, seven out of 19 sponsors are from China. One of them is Wanda Group, a real estate and leisure conglomerate, which went for FIFA’s top roster of sponsors alongside other newcomers such as Middle East's Qatar Airways and Russian state oil giant Gazprom. The Chinese conglomerate will have full access to the advertising and marketing of all events over the next four World Cups, starting with 2018.

The second group of tournament-only sponsors lists three brands from the Far East. Besides established names such as Budweiser and McDonalds, FIFA appointed TV and refridgerator manufacturer Hisense, smartphone developer Vivo, and dairy firm Mengniu as second-tier partners.

Vivo, only founded nine years ago, reportedly paid €400m for a six-year deal that included Russia 2018, Qatar 2022 as well as the Confederations Cup. Mengniu, the country’s second-largest dairy company, was granted the right to air commercials across a total of 64 World Cup games in June and July 2018.

Even though the Regional Supporters category invariably attracts local companies (2018: 4 Russian companies; 2014 6 Brazilian), this did not deter China’s electric scooter company Yadea, technology and entertainment company Luci and mens clothing brand Diking from becoming World Cup sponsors.

China’s commitment to the World Cup in Russia is part of the country’s awareness raising campaign, following comments by President Xi Jinping who wants China to become a football superpower by 2050. It could also be interpreted as a bid to help its plans to host, and ultimately win, a FIFA World Cup within the next 15 years.

Broadcasting

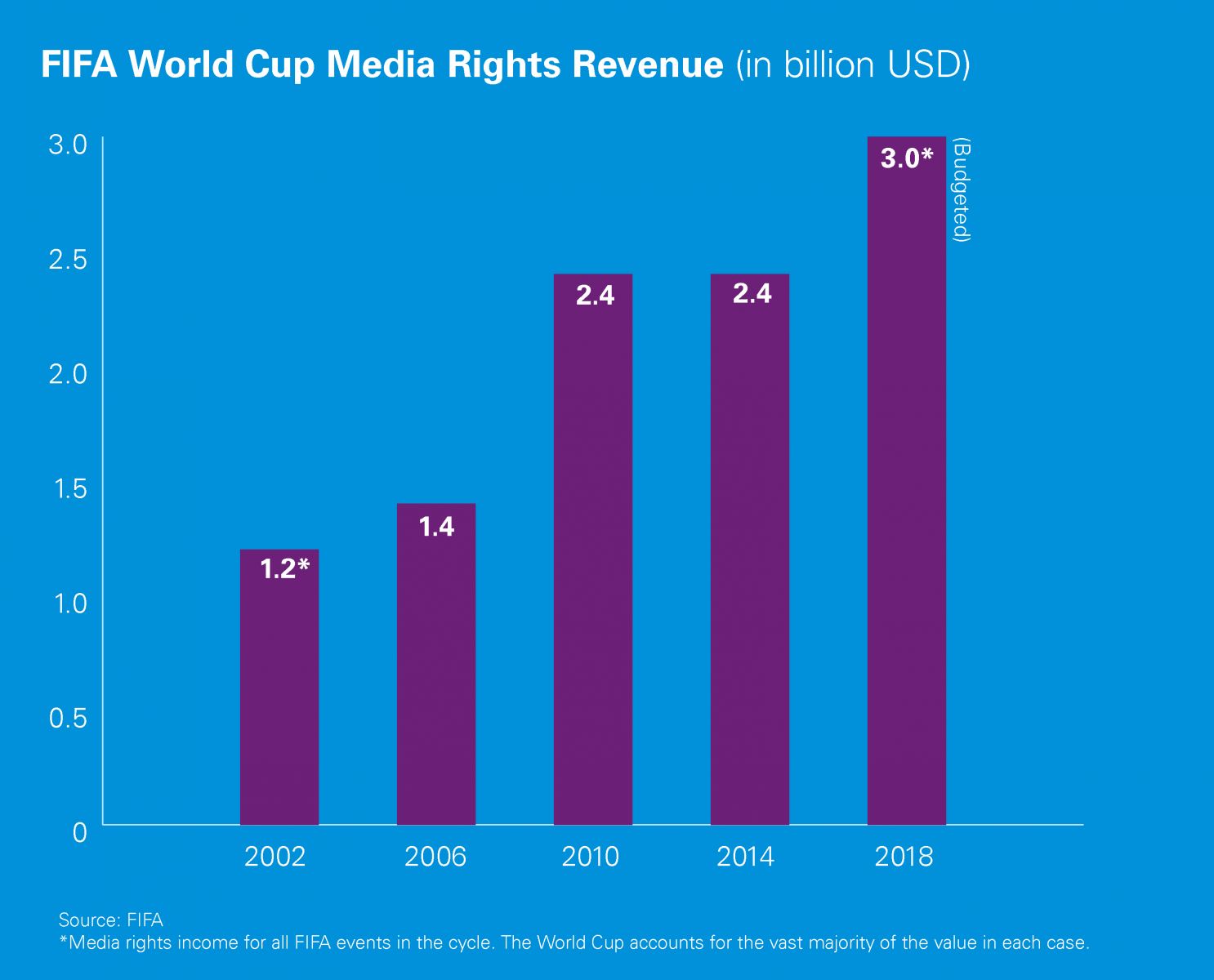

The FIFA World Cup was first broadcast on television in 1954 and is now the most widely viewed and followed sporting event in the world, exceeding even the Olympic Games. According to FIFA, more than one billion fans tuned-in to watch the final of the 2014 World Cup in Brazil. As we can gather from the graph, FIFA’s revenues from media rights have been growing substantially, doubling income from $1.2bn in 2002 to $2.4bn in 2014.

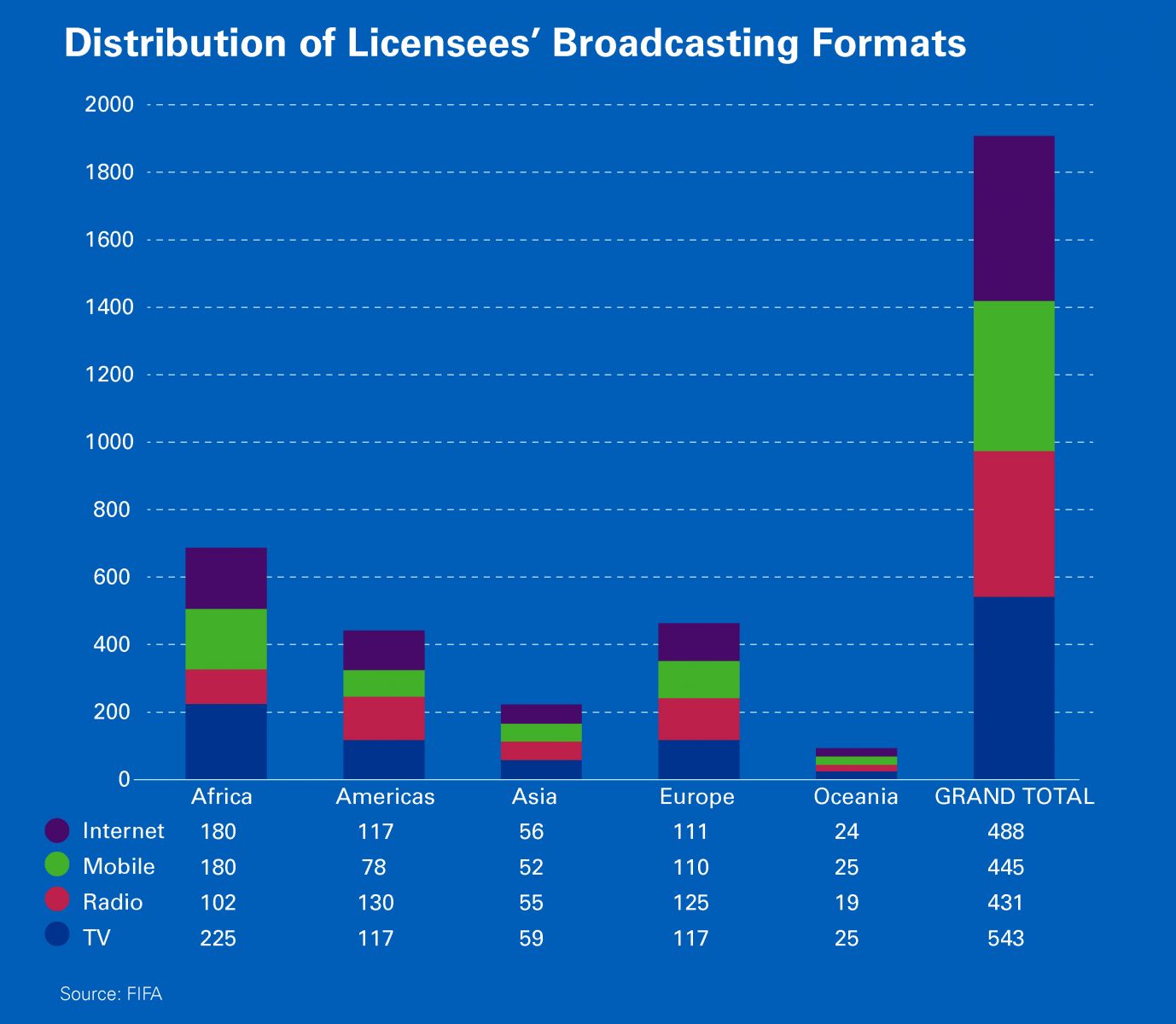

For this year’s tournament, the broadcasting rights for the 2018 competition have been sold directly or through licensed companies (licensors) to a total of 217 territories across five different regions (Africa, Americas, Asia, Europe and Oceania). The majority of territories are located in Europe (55), closely followed by Africa (54). In total, 685 licensees aquired the media rights for this year’s World Cup. The majority of licensees that bought the FIFA rights are from Africa (274), followed by Europe (175) with Asia accounting for just 59 outlets. This is also due to the fact that all of China’s FIFA rights are owned and controlled by CCTV who sublicensed rights to only two other outlets.

Among the broadcasting rights distributed, FIFA distinguishes between TV, Radio, Mobile and Internet. It is interesting to note that the number of traditional broadcasting formats (TV and radio) is comparable to the share of digital broadcasting (Mobile and Internet), which demonstrates the growing importance of streaming platforms. Out of all regions, Africa acquired the biggest share of Mobile/Internet licensing formats.

FIFA sold the first rights package for Russia 2018 to BeIn Sport (at the time, Al Jazeera) seven years ago. Since then, the usual collection of international broadcasters have obtained rights including CCTV in China, Fox and Telemundo in the United States, DirecTV in the Caribbean and the European Broadcasting Union (EBU) across 37 territories. Ironically, it was only end of last year that the host country’s media outlets Channel One, RTR and Match TV agreed to split coverage of the competition in a protracted negotiation process that asked for a fee three times the amount spent on the 2014 rights ($40 million).

For a few outlets the investments might not necessarily pay off. Fox Sports had reportedly paid a record $400 million to take over the English-language rights to the 2018 and 2022 World Cups from Walt Disney Co.’s ESPN/ABC, but the US Soccer Team failed to qualify for the tournament. The same applies for Italy’s Mediaset, who acquired the exclusive broadcast rights for a reported fee of $93 million. China (CCTV), also not taking part in the competition, paid between $300 and $400 million to secure the rights for 2018 and 2022. CCTV then went on to sell the digital rights to streaming platforms Migu (owned by mobile carrier China Mobile) and Youku (Alibaba-owned).

Telemundo, the Spanish-language broadcast network owned by NBCUniversal also made a heavy investment. It paid about $600 million for the 2018 and 2022 competitions, outbidding Univision Communications Inc., who had aired the World Cup since 1970.

The World Cup will, as ever, captivate TV audiences across the globe. The appeal of the game, coupled with the commercial opportunities that have emerged over the past decade, have transformed FIFA’s flagship competition into a huge and lucrative business venture that has no equals in international sport. Despite all controversies surrounding the football governing body, it appears that the tournament format can still attract a substantial number of sponsors and broadcasters. As soon as 2018 is over and the iconic trophy is raised by the winners, the machine will have already moved on to 2022.